Revisiting the Green Climate Fund in the Pacific

Georgia Hammersley and Roland Rajah

2023-04-19

AUSTRALIA

ENERGY AND ENVIRONMENT

This article orginally appeared in The Interpreter published by the Lowy Institute

Global climate funds have faced much criticism for failing to deliver fast and flexibly enough to match the urgency of the climate crisis, especially for the world’s most climate vulnerable countries.

In the Pacific, the Green Climate Fund (GCF) – the world’s largest climate-dedicated fund – is generally seen as slow and difficult to work with. Australia, the Pacific’s largest donor, committed an initial US$187 million to the GCF and served as co-chair of its board. But the previous Australian government withdrew its involvement in 2018, citing governance and operational challenges and stating it would instead provide its climate financing through bilateral channels.

This year, the GCF is looking to raise funds for its second financial replenishment covering 2024–27. As the climate crisis escalates, it is worth revisiting the role of the GCF in the Pacific.

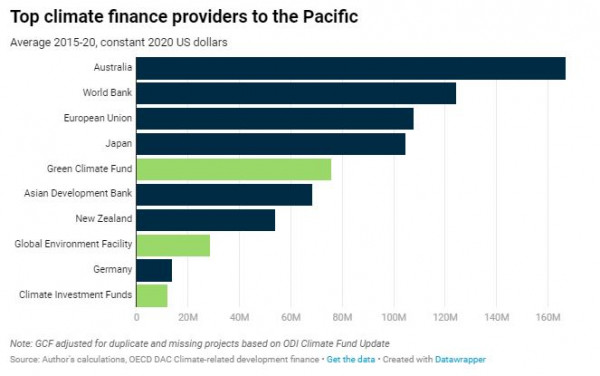

Contrary to the story of substantial underperformance, the GCF and other climate funds stack up relatively well compared to other climate finance providers in the Pacific. The GCF is now the fifth-largest source of all climate finance in the region. On average, the GCF approved US$76 million in Pacific projects each year from 2015 (when the GCF was operationalised) to 2020 (the latest year of comparative climate finance data from the OECD). The Green Environment Facility and the Climate Investment Funds are also among the top ten climate finance providers in the Pacific, with the Adaptation Fund coming in at sixteenth.

Collectively, these four global climate funds provided about US$120 million a year, or almost 15% of all Pacific climate finance, during 2015–20 – roughly as much as the World Bank and not too far behind Australia as the region’s leading climate finance provider, averaging US$167 million a year.

To be clear, the total volume of Pacific climate finance from all parties remains well below what’s required. The International Monetary Fund for instance estimates the region requires additional climate financing of US$1 billion a year or 6.5–9% of regional GDP.

However, when comparing the contributions of the GCF and other climate funds to the Pacific’s major climate finance providers, it is hard to argue that they have been massively underperforming. It is also fair to say that the GCF has been making a substantial difference in the most climate-exposed Pacific countries.

Tuvalu has for instance secured significant financing for much needed coastal protection infrastructure, equal to around 12% of GDP a year over 2015–22. GCF financing is also substantial at 2–4% of GDP in Kiribati, Nauru and Marshall Islands. Elsewhere, Tonga, Solomon Islands, Samoa, Micronesia and Vanuatu have received smaller proportional financing at 1–2% of GDP, but enough that the GCF can claim to be making a material contribution.

However, despite this relatively positive picture, Pacific countries continue to face significant barriers in accessing the GCF.

In particular, the Fund’s accreditation and project approval procedures heavily disadvantage small island developing states – where the ability to meet stringent public financial management requirements is limited, human capacity is already stretched thin, and project size tends to be small relative to the high transaction costs involved.

Pacific countries retain a strong preference for direct access to GCF financing. Most have made substantial efforts to become accredited with the GCF for such access, reflecting a desire for greater country control, building their own capacity, and ensuring the needs of local communities are adequately prioritised.

To date, only Fiji and Cook Islands have been successfully accredited for GCF direct access. So far, neither have received any disbursements, though the GCF approved a US$10 million Agrophotovoltaic Project for Fiji in 2020.

The vast majority of GCF financing to the Pacific has instead continued to go through indirect access, notably via projects delivered by the Asian Development Bank and World Bank, which together account for 95% of GCF project disbursements in the region. The remaining 5% has gone through Pacific regional organisations.

Critically, challenges are not only about direct versus indirect access but also about the overall volume of GCF financing.

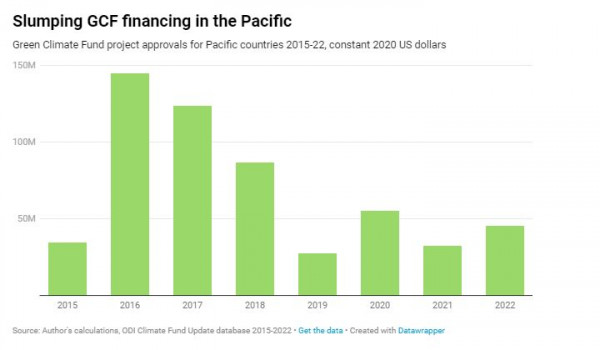

A concerning trend is that GCF project approvals for the Pacific have slumped dramatically in recent years. GCF project approvals averaged almost US$100 million a year during 2015–18 but have since fallen by almost 60% to just US$41 million a year during 2019–22 (see chart).

Year-to-year figures are heavily influenced by when large individual projects are approved, so it can be difficult to discern the underlying trend. The Covid-19 pandemic is also likely to have significantly affected project preparation pipelines.

It is also important to recognise that, even at the recent lower levels, the GCF is still among the Pacific’s top climate finance providers.

Nonetheless, the decline in new Pacific projects is concerning, especially given GCF financing to the rest of the world has greatly accelerated since 2019 when the GCF moved from consensus to majority-based decision making. Global GCF project approvals have increased by more than 40% since 2018, as opposed to the almost 60% reduction observed for the Pacific.

It is also notable that the slowdown in Pacific approvals and its divergence with the accelerating global trend have coincided with Australia’s 2018 exit – raising the prospect that the loss of the region’s main donor advocate has had a major impact on the Pacific’s ability to access the GCF.

Unlike many other multilateral institutions, the GCF does not have a set formula for determining country allocations. It could only help having Australia back at the table advocating for both specific Pacific projects and deeper structural changes to improve access for small island states.

The Albanese government is emphasising its climate credentials at home, in the Pacific, and globally. It is also bidding to co-host the COP Climate Summit in 2026 together with Pacific nations. With the GCF’s next replenishment coming up at the end of this year, now is the time for Australia to rethink its participation in the world’s most important global climate fund.

Membership

NZIIA membership is open to anyone interested in understanding the importance of global affairs to the political and economic well-being of New Zealand.